- The Money Trails

- Posts

- How Private Equity Is Eating Away America’s Retirement

How Private Equity Is Eating Away America’s Retirement

Inside the private equity takeover of America's retirement savings

Kartik Vyas & Gen Kimura

November 20, 2025

|  |  |

What’s in This Week’s Issue…

Good morning. America’s retirement system was supposed to represent safety, a future you can count on. But right now, that future is being quietly rewritten.

Not by Congress. Not by regulators.

But by a small circle of private equity firms who’ve discovered a loophole so powerful it lets them move billions of dollars of American retirement savings offshore, out of U.S. protections and into complex, high-risk bets that almost no one can see.

So this week…

🏆 The Big Play: How private equity quietly took control of retirement and moved it offshore

💪 The Power Move: How to protect yourself when the “safe bucket” of the economy stops being safe

💵 Follow the Money: Is the Trump Administration shielding Andrew Tate from investigation?

-GEN

🏆 The Big Play

The biggest money power story of the week.

The Great Offshoring: How Private Equity Is Quietly Eating America’s Retirement

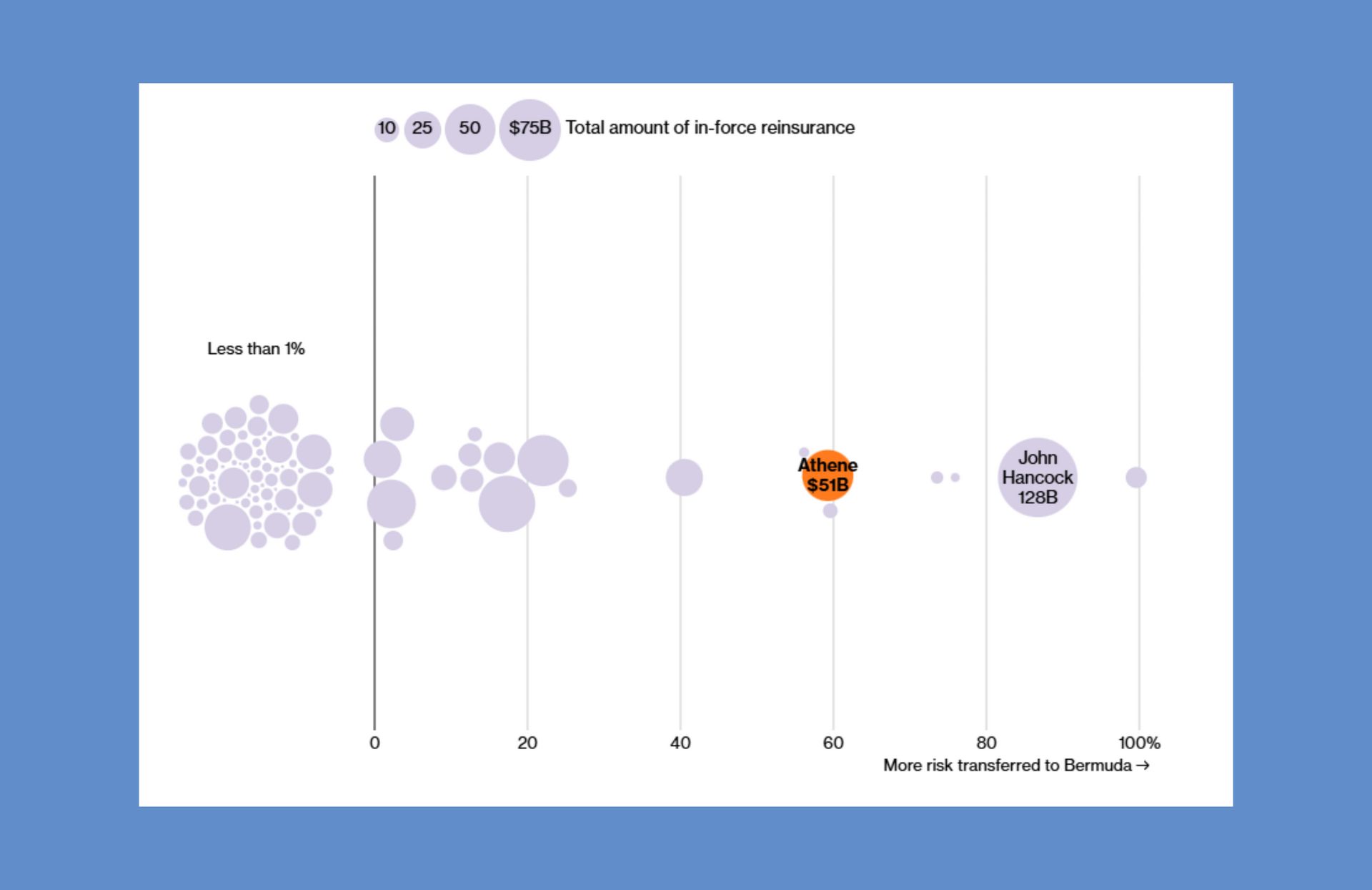

Reinsurance 101

Retirement money was always the boring corner of finance: insurers invested it safely, regulators watched it closely, and retirees expected a predictable check.

But that world is collapsing. A quiet structural shift that started after 2008 is now accelerating so fast that regulators themselves are struggling to keep up.

And to understand how deep this shift is, you have to start at the very beginning:

1. The Silent Buyout of Retirement

For most of modern financial history, insurance companies were some of the safest, most regulated institutions in America.

But after the financial crisis, insurers struggled with a low-interest-rate environment that made long-term guarantees extremely expensive to honor.

And that’s where private equity stepped in with a model that solved every insurer’s biggest problem.

Firms like Apollo, KKR, Blackstone, Brookfield, and Carlyle started buying insurers outright or partnering with them to manage their assets.

Why?

Because insurers sit on massive piles of “patient capital” (annuities and life insurance premiums) that don’t need to be paid out immediately. This is the perfect raw material for private equity.

And the moment they got control, the business model flipped:

Traditional insurers invested conservatively for stability.

Private equity–owned insurers invested aggressively for yield.

But the most powerful financial engineering wasn’t happening inside the U.S. It was happening outside it.

2. The Bermuda Escape Hatch

Bermuda isn’t just a tropical island. It’s a regulatory advantage.

Under U.S. rules, insurers must hold thick capital buffers, disclose their risks, and value assets conservatively. On the contrary, Bermuda allows thinner cushions, looser models, and far more discretion in valuing complex assets.

So private equity firms created (or acquired) Bermuda-based reinsurance subsidiaries. Then they started moving hundreds of billions of U.S. retirement dollars into these offshore vehicles.

Here’s why that matters:

When a U.S. insurer “reinsures” its liabilities with its own Bermuda affiliate, it moves both the obligation and the regulatory oversight out of America.

On paper, everything looks compliant. In reality, the risk profile of millions of retirees is being reshaped offshore.

And because Bermuda’s rules allow more aggressive investment strategies, these firms can use retirement savings to pursue private credit, real estate debt, and even long-dated private equity positions.

In short, retirement money becomes the fuel for Wall Street’s highest-return, highest-risk strategies, with everyone struggling to see what’s actually happening inside these offshore books.

None of this violates the law. But it rewrites the nature of what “safe money” means.

And it sets up the most dangerous dynamic of all.

3. When Complexity Becomes the Risk

The biggest danger in finance isn’t always leverage. It’s opacity.

And today, the retirement system has never been more opaque:

Regulators can’t easily see inside Bermuda vehicles

Rating agencies rely on models built by the same firms they’re rating

Insurers increasingly use illiquid, hard-to-value assets

Consumers have no visibility into how their own pensions are being invested

The result?

You get a system that looks stable from the outside but is now structurally dependent on private equity’s ability to generate high returns with low transparency, forever.

Think back to 2008.

The crisis didn’t start because people understood the risks. It started because they didn’t.

Today’s system echoes that pattern: long-dated promises backed by complex structures most people don’t get to see.

And when the incentive structure rewards opacity, financial engineering, and yield-hunting over safety, the real question becomes:

What happens when the retirement system built on “safety” quietly becomes one of the biggest speculative engines in the economy?

💪 The Power Moves

Playbook for understanding the game of power.

The Only Way to Survive When the “Safe Bucket” Stops Being Safe

How insurance companies transfer risk to Bermuda for higher returns

There’s a pattern in every financial story we cover:

Whenever a system becomes too complex for ordinary people to understand, someone somewhere is making money off that complexity.

Retirement is no different.

The safest savings Americans have are now exposed to risks they never signed up for, not because they wanted higher returns, but because private equity decided those savings were the perfect fuel for their next phase of growth.

So, don’t assume the safest parts of the system are actually safe. Understand what you own and who controls the risk behind it.

The Takeaway:

When Wall Street starts treating retirement savings like a new asset class to engineer, the smartest move isn’t to chase the yield.

It’s to anchor your future in what complexity can’t distort: transparency, simplicity, and ownership you can actually see.

💵 Following the Money

Three of the wildest financial and corruption stories from around the world.

Tate brothers

✨ Poll time!

Do you think the average American truly understands how much of their retirement savings is now controlled by private equity firms? |